An Early Warning System for Equity Risk

Through exogenous shock channels and network analytics

Managing equity risk means living with a permanently noisy information channel, where endogenous shock divergence rates spike constantly. Distinguishing alerts worth acting on from those that resolve themselves is one of the hardest problems in practical risk management.

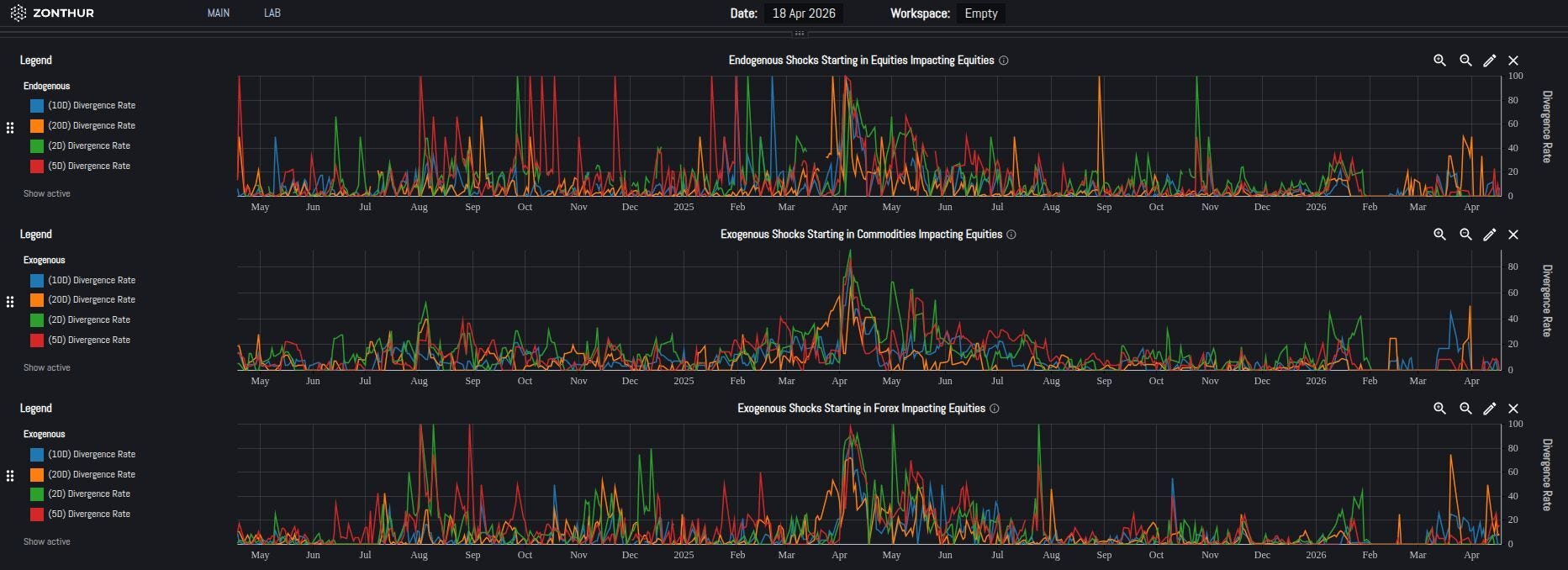

The three charts above track divergence rates across two years and three shock channels for equities. A rising divergence rate reflects periods of elevated expected volatility, not necessarily higher directional conviction. Endogenous shocks originate within equity markets themselves, while exogenous shocks originate in other asset classes - here, Commodities and Forex - and propagate into equities.

Monitoring exogenous shock channels alongside the endogenous one addresses the noise problem in two ways.

First, as a conviction filter. Forex and Commodity markets are more directly tethered to the macro forces that drive systemic stress (like trade flows, monetary policy, geopolitical disruption) and have less of the sentiment and flow dynamics that amplify noise in equity markets. When Commodity or Forex shock, divergence rates spike into equities, the signal carries more macro weight, and warrants a different level of attention than the same reading in the endogenous channel.

Second, and more importantly, as an early warning system. For example, the Commodity channel began registering elevated divergence rates in March 2025, weeks before the equity dislocation that followed Liberation Day. Whether commodity markets were pricing the macro implications of political developments faster than equities, or whether underlying disturbances were already building independently, the practical conclusion is the same: the signal was there earlier, in a different market.

The nature of a shock determines where it becomes visible first. Macro shocks with commodity or currency transmission signatures will show up in those channels before equities fully price them. Monitoring only the endogenous equity channel means you are, by construction, always the last to know.

The Forex channel into equities was elevated across multiple time horizons as of April 18, 2026.

Improving Signal-to-Noise Ratio

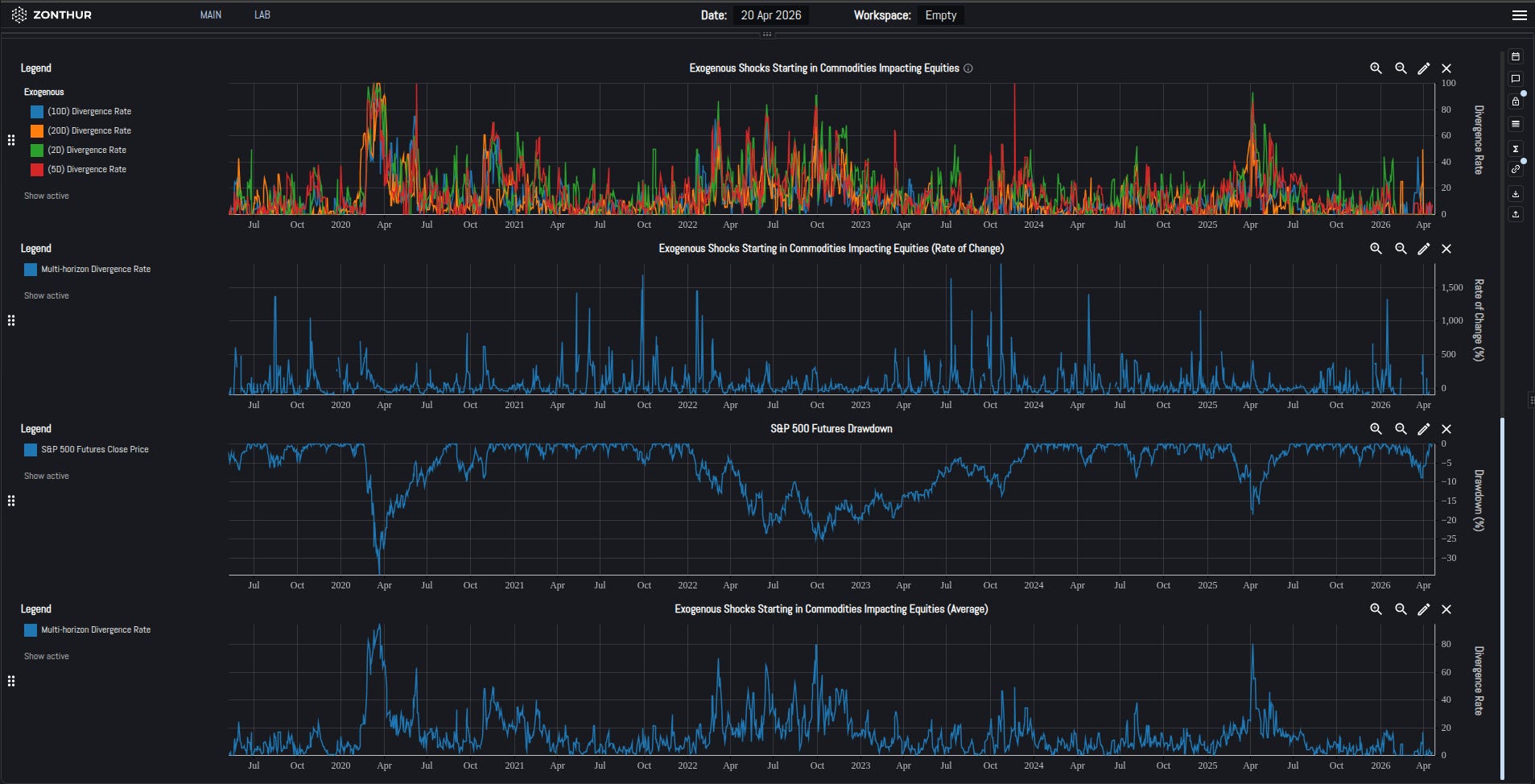

A natural follow-up question is how often the Commodity divergence rate elevates, and how reliably it precedes an equity dislocation. Although a few cases are suggestive, the signal-to-noise ratio is what determines whether it's a usable early warning.

The raw divergence rate fires regularly enough that treating every spike as an actionable alert would be operationally untenable, but that's not the right metric for early warning purposes. The rate of change of the multi-horizon average is considerably more selective, as it measures whether commodity shocks are accelerating, not merely whether they are elevated.

Over six years, major spikes in that rate of change have preceded or coincided with every significant S&P 500 Futures drawdown in the dataset: for example, April 2020, the 2022 bear market, and Liberation Day in April 2025. The current reading is among the largest in the six-year history.

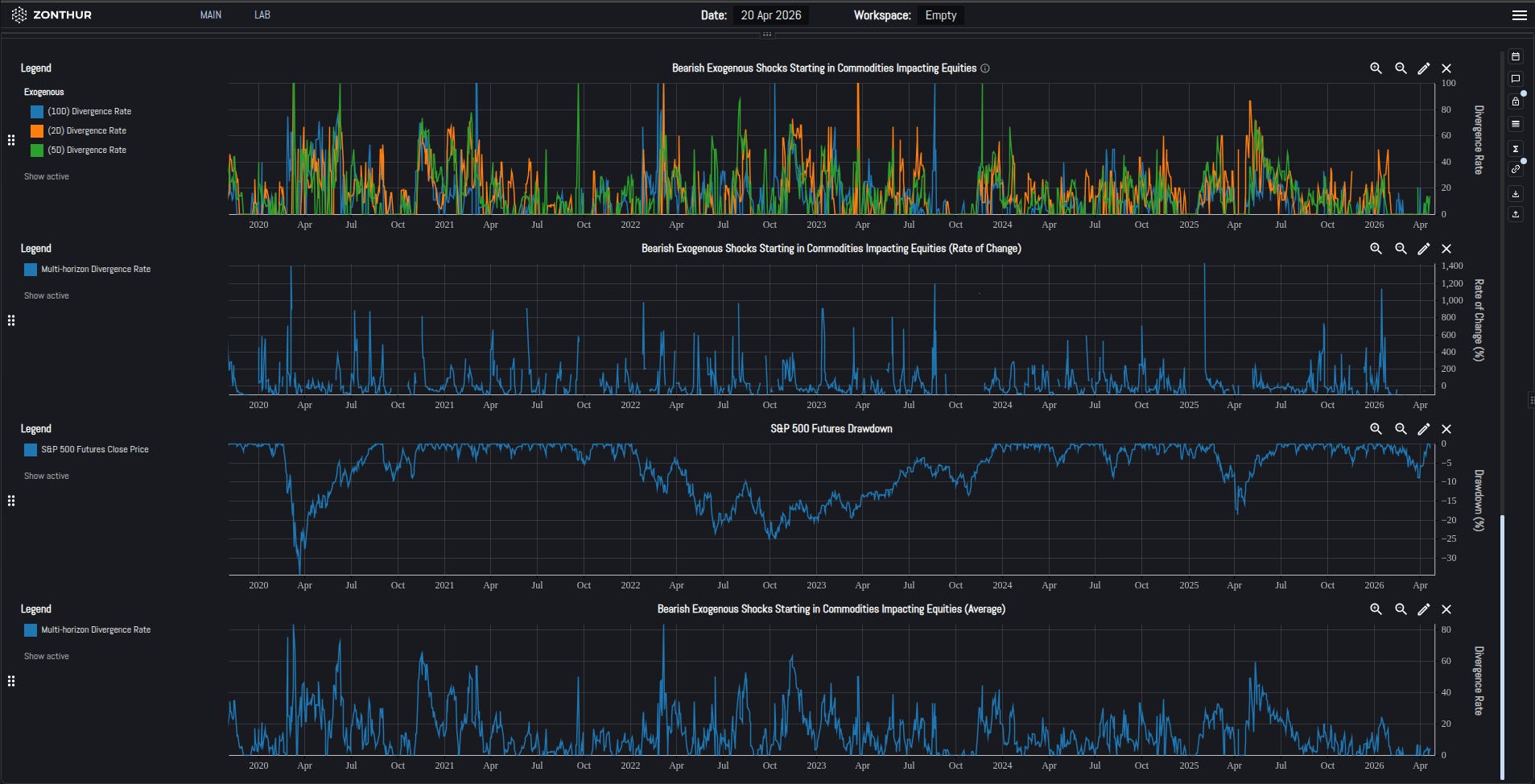

Filtering further to bearish commodity shocks specifically (those with a directionally negative impact into equities) sharpens the picture considerably. With the noise dropping during benign periods, the signal during genuine stress episodes becomes cleaner.

Two qualifications are worth stating explicitly.

The signal identifies stress transmission, not magnitude. For conviction on scale it needs to be read alongside other channels.

The broad Commodity → Equity channel shown here is one of many exogenous shock types Zonthur tracks, which can be segmented more narrowly or broadly by asset class, equity universe, or time horizon. A more targeted segmentation typically sharpens the leading properties further.

Final Thoughts

To build most equity risk frameworks around the equity market itself (e.g. its prices, its volatility, its history) is a reasonable starting point but by the time stress is visible on the endogenous channel, it might have already propagated through other markets. Commodity, currency markets, or fixed income likely have already priced something.

The central point here is not to present exogenous shock channels as perfect early warning systems, because they aren’t. The distinction is whether you see what other markets are pricing before equities catch up, or only after.

Disclaimer: The information provided in this content is for general informational purposes only and does not constitute investment, financial, legal, tax, or other professional advice. It should not be relied upon as such. Always consult with a qualified professional or advisor before making any investment or financial decisions.